Vail Resorts Reports Second Quarter Fiscal 2026 Results and Provides Updated Fiscal 2026 GuidanceVail Resorts, Inc.Ā reported results for the second quarter of fiscal 2026 ended January 31, 2026 and provided the Company's ski season-to-date metrics through March 1, 2026. Highlights

Commenting on the Company's fiscal 2026 second quarter results, Rob Katz, Chief Executive Officer said, "This has been the most challenging winter across the Rockies that we have ever experienced with the lowest snowfall levels in more than 30 years for our Colorado and Utah resorts, combined with warmer temperatures, resulting in reduced terrain throughout the quarter and into February. Given that backdrop, we are pleased with the strength and stability shown by our operating model, as we reported only modest declines in lift revenue in what many would consider a worst-case weather scenario. While these conditions and the resulting visitation headwinds negatively impacted our quarterly results, we remained focused on the areas within our control. This includes our advanced commitment strategy, continued investments in our resorts and our employees, and progressing key initiatives to optimize visitation, including enhanced marketing and new products. I especially want to recognize the exceptional execution delivered by our teams over the course of the season, resulting in record high enterprise guest satisfaction scores, including increases over prior year in both Colorado and Utah despite conditions, along with continued progress on our transformation plan. I am confident that with our collective strength and focus, we will continue to elevate the guest experience and deliver sustainable long-term value for shareholders." Second Quarter Operating Results

Season-to-Date Metrics through March 1, 2026Ā The Company reported certain ski season metrics for the comparative periods from the beginning of the ski season through March 1, 2026, and for the same prior year period through March 2, 2025. The reported ski season metrics are for the Company's North American destination mountain resorts and regional ski areas, excluding the results of the Australian and European resorts and ski areas in both periods. The data mentioned below is interim period data and is subject to fiscal quarter end review and adjustments.

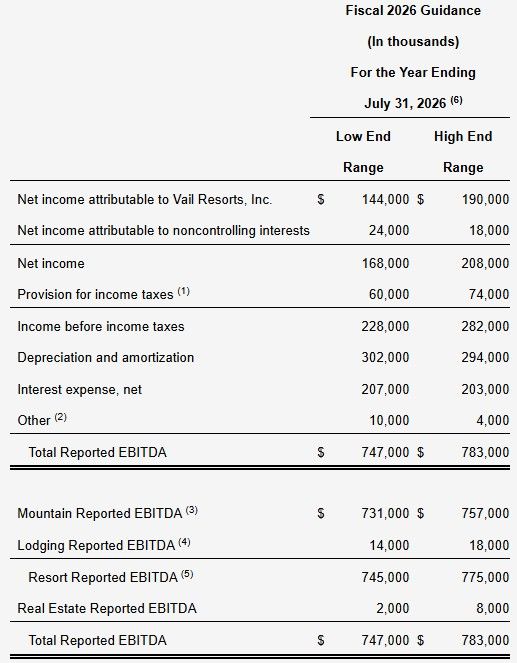

Fiscal Year 2026 Guidance Commenting on Fiscal 2026 guidance, Katz said "Due to the persistent, historically challenging weather conditions in the Rockies, which continued to limit terrain availability, the Company is reducing its fiscal 2026 guidance. While we are lowering our estimates for the fiscal year, given the unprecedented weather in the Rockies, the impact from conditions was mitigated by our advance commitment strategy and resource transformation efforts. We are proud of the resilience of the business model and execution of our teams at our resorts that are delivering on the experience for our guests." The Company now expects fiscal 2026 Net Income and Resort EBITDA guidance as follows:

Given ongoing variable conditions in the Rockies, there may be greater variability of results; current guidance assumes (1) the Company's estimate of conditions between now and the remainder of the season staying consistent in North America; (2) normal weather conditions for the 2026 Australian ski season; (3) continuation of the current economic environment; and (4) foreign currency exchange rates as of March 6, 2026, including an exchange rate of $0.73 between the Canadian Dollar and U.S. Dollar related to the operations of Whistler Blackcomb in Canada, an exchange rate of $0.70 between the Australian Dollar and U.S. Dollar related to the operations of Perisher, Falls Creek and Hotham in Australia, and an exchange rate of $1.28 between the Swiss Franc and U.S. Dollar related to the operations of Andermatt-Sedrun and Crans Montana in Switzerland, and does not include any potential impacts related to future fluctuations in foreign currency exchange rates, which may be impacted by tariffs, trade disputes, or other factors. The following table reflects the forecasted guidance range for the Company's fiscal year ending July 31, 2026 for Total Reported EBITDA (after stock-based compensation expense) and reconciles net income attributable to Vail Resorts, Inc. guidance to such Total Reported EBITDA guidance. Liquidity and Return of Capital Despite difficult conditions this year, the Company remains confident in the long-term strong cash flow generation capabilities of our Company and its stable business model.

|

|

ropeways.net | Home | Economy | 2026-03-12

Back

Back Add Photos

Add Photos Print

PrintMore articles:

Black Mountain Abandons Co-op Plans

2026-03-23

Mountain Planet: Mountains: Design, a New Driver of Cable Mobility in Mountain Regions

2026-03-20

Powder Mountain: New lifts, more terrain, unbelievably uncrowded skiing

2026-03-19

Google Adsense