Vail Resorts Reports Fiscal 2024 Third Quarter ResultsProvides Updated Fiscal 2024 Guidance, and Provides Early Season Pass Sales Results Vail Resorts, Inc. reported results for the third quarter of fiscal 2024 ended April 30, 2024, reported early season pass sales, updated fiscal 2024 guidance, and announced share repurchases completed during the quarter. Highlights

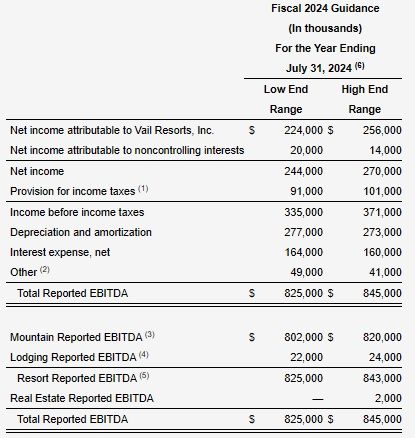

Commenting on the Company's fiscal 2024 third quarter results, Kirsten Lynch, Chief Executive Officer, said, "Given the unfavorable conditions across our North American resorts for a large portion of the 2023/2024 North American ski season, we were pleased to see improved results in March and April, with visitation across our western North American resorts in particular benefiting from improved conditions. While pass product visitation returned as expected, as we communicated in April, lift ticket visitation did not return to typical historical guest behavior for the spring, primarily at Whistler Blackcomb, which was down significantly relative to the prior year period. Despite these challenges, the Company grew resort net revenue and Resort Reported EBITDA to record levels in the third quarter, supported by the stability created from our advance commitment strategy, operations executional excellence, and continued strong growth in ancillary spending per skier visit across our ski school, dining, and rental businesses at our resorts. "Our results throughout the 2023/2024 North American ski season highlight both the stability provided by our season pass program and the investments we have made in our resorts and employees. The winter season included significant weather-related challenges, with approximately 28% lower snowfall for the full winter season across our western North American resorts compared to the same period in the prior year and limited natural snow and variable temperatures at our Eastern U.S. resorts (comprising the Midwest, Mid-Atlantic, and Northeast). For the 2023/2024 North American and European ski season, total skier visits declined 7.7% as compared to the prior year period, which we believe was driven by a combination of unfavorable conditions and broader industry normalization post-COVID following record visitation in the U.S. during the 2022/2023 ski season. Skier visitation from lift ticket guests was particularly impacted, declining 17% compared to the prior year period. Despite the decline in visitation, ancillary spending was strong across our ski school, dining, and rental businesses at our resorts. Resort net revenue for the second and third quarter combined period increased 1% and Resort Reported EBITDA increased 6% over the prior year, supported by our advance commitment strategy, strong growth in guest ancillary spending per visit, and continued cost discipline." Regarding the outlook for fiscal 2024, Lynch said, "While late season results improved, we now expect Resort Reported EBITDA to be between $833 million and $851 million on a comparable basis with our prior guidance issued March 11, 2024, which included $4 million of acquisition related expenses specific to Crans-Montana, but excluded closing costs, operating results, and integration expenses associated with Crans-Montana. The reduction relative to the guidance provided on March 11, 2024 is primarily from lift ticket visitation not returning to typical historical spring behavior as expected in the March and April period, primarily at Whistler Blackcomb, along with lowered expectations for the fourth quarter of $9 million primarily related to the demand outlook for our Australian resorts. In addition, with the closing of the acquisition, we now expect Crans-Montana to contribute negative $12 million of Resort Reported EBITDA for fiscal 2024, including negative $9 million from acquisition, closing, and integration expenses and negative $3 million from operating results in the fourth quarter. Including the full impact of Crans-Montana, the Company now expects net income attributable to Vail Resorts, Inc. to be between $224 million and $256 million and Resort Reported EBITDA to be between $825 million and $843 million." Operating Results A more complete discussion of our operating results can be found within the Management's Discussion and Analysis of Financial Condition and Results of Operations section of the Company's Form 10-Q for the third fiscal quarter ended April 30, 2024, which was filed today with the Securities and Exchange Commission. The following are segment highlights: Mountain Segment

Lodging Segment

Resort - Combination of Mountain and Lodging Segments

Total Performance

Liquidity and Capital Structure Update Commenting on capital allocation, Lynch said, "Our balance sheet remains strong, including total cash and revolver availability as of April 30, 2024 of approximately $1.3 billion, with $705 million of cash on hand, $409 million of U.S. revolver availability under the Vail Holdings Credit Agreement and $216 million of revolver availability under the Whistler Credit Agreement. As of April 30, 2024, our Net Debt was 2.4 times trailing twelve months Total Reported EBITDA. On May 8, 2024, we completed an offering of $600 million aggregate principal amount of 6.50% Senior Notes due 2032, and used the net proceeds from these notes to fund the redemption of the entire amount of $600 million 6.25% Senior Notes due 2025 on May 15, 2024. Additionally, the Company completed an amendment of its Vail Holdings Credit Agreement to extend the maturity of the $969 million term loan and $500 million revolver from 2026 to 2029. The Company repurchased approximately 0.3 million shares at an average price of approximately $217 for a total of $75.0 million during the quarter. For the nine months ended April 30, 2024, the Company repurchased 0.6 million shares for approximately $125 million. We have approximately 0.8 million shares remaining under our authorization for share repurchases and remain focused on returning capital to shareholders while always prioritizing the long-term value of our shares. Additionally, the Company declared a quarterly cash dividend on Vail Resorts' common stock of $2.22 per share. The dividend will be payable on July 10, 2024 to shareholders of record as of June 25, 2024. We will continue to be disciplined stewards of our capital and remain committed to prioritizing investments in our guest and employee experience, high-return capital projects, strategic acquisition opportunities such as the recent addition of Crans-Montana, and returning capital to our shareholders through our quarterly dividend and share repurchase program." Crans-Montana Mountain Resort As previously announced, on May 2, 2024, the Company closed on the purchase of its second European resort acquisition, Crans-Montana, for a purchase price of CHF 97.2 million ($106.8 million), after adjustments for certain agreed-upon items, including a CHF 4 million reduction in the purchase price to account for timing of closing after the winter season. The Company acquired an 84-percent ownership stake in Remontées Mécaniques Crans Montana Aminona (CMA) SA, which controls and operates all the resort's lifts and supporting mountain operations, including four retail and rental locations. The Company also acquired full ownership of SportLife AG (increased from the previously announced 80% ownership stake), which operates one of the ski schools located at the resort, and full ownership of 11 restaurants located on and around the mountain. This world-class resort spans over 1,400 meters (approximately 4,593 feet) of skiable vertical terrain and 140 kilometers (approximately 87 miles) of trails. Located in the Valais canton of Switzerland, Crans-Montana is approximately two and a half hours from Geneva and less than four hours from Milan and Zurich. The valuation for the entirety of the resort operations was CHF 118.5 million, including approximately CHF 7 million of debt that will remain in place and adjusted for purchase price adjustments to account for seasonality and closing timing. Vail Resorts anticipates that the resort will generate approximately CHF 5 million of Resort Reported EBITDA in its fiscal year ending July 31, 2025, the first full year of operations under the Company's ownership. We expect significant EBITDA growth over time from the inclusion of the resort on the Epic Pass products, network synergy, and investments in the guest experience. Subject to the timing of capital project approvals and completion, Vail Resorts is planning to invest approximately CHF 30 million over the next five years in one-time capital spending to elevate the guest experience. Normal annual maintenance capital spending is expected to be approximately CHF 3 million. Capital Investments Regarding calendar year 2024 capital expenditures, Lynch said, "As previously announced, we expect our capital plan for calendar year 2024 to be approximately $189 million to $194 million, excluding $13 million of incremental capital investments in premium fleet and fulfillment infrastructure to support the official launch of My Epic Gear for the 2024/2025 winter season at 12 destination and regional resorts across North America, $11 million of growth capital investments at Andermatt-Sedrun, $1 million of reimbursable capital, and investments at Crans-Montana, which we expect will include $3 million of maintenance capital expenditures and $2 million associated with integration activities at Crans-Montana. Including My Epic Gear premium fleet, fulfillment infrastructure capital, one-time investments, and investments at Crans-Montana, our total capital plan for calendar year 2024 is now expected to be approximately $219 million to $224 million." Season Pass Sales Commenting on the Company's season pass sales for the upcoming 2024/2025 North American ski season, Lynch said, "Pass product sales through May 28, 2024 for the upcoming North American ski season decreased approximately 5% in units and increased approximately 1% in sales dollars as compared to the period in the prior year through May 30, 2023. Pass sales dollars are benefiting from the 8% price increase relative to the 2023/2024 season, partially offset by the mix impact from the growth of Epic Day Pass products. Pass product sales are adjusted to eliminate the impact of foreign currency by applying an exchange rate of $0.73 between the Canadian dollar and U.S. dollar in both periods for Whistler Blackcomb pass sales." Lynch continued, "Pass product sales for this past season, the 2023/2024 North American ski season, had grown 62% in units and 43% in sales dollars over the past three years. Since the pass price reset in the spring of 2021, we have increased pass product pricing 25% through spring 2024. We believe the spring pass results for guests committing for winter 2024/2025 were impacted by the industry decline in visitation following a record 2022/2023 U.S. ski season. The decline in units relative to the prior year season to date results was primarily driven by a decline in new pass holders. The primary source of new pass holders in the spring are lift ticket guests that visited in the prior winter season. This past season, lift ticket visitation declined due to weather, and did not fully return to typical behavior after conditions improved, creating a smaller audience as the primary source of new pass holders in the spring. For renewing pass holders, the Company achieved strong unit growth among the Company's most loyal, tenured renewing pass holders (those who have had a pass for three years or more). Spring renewals for lower tenured pass holders (first time and second year pass holders) demonstrated lower renewal rates in the spring, which may reflect delayed decision making to the fall. Overall renewing pass holder product net migration was positive, and Epic Day Pass products experienced modest unit growth driven by the strength in renewing pass holders. "The majority of our pass selling season is ahead of us, and we believe the full year pass unit and sales dollar trends will be relatively stable with the spring results. We will provide more information about our pass sales results in our September 2024 earnings release." Regarding Epic Australia Pass sales, Lynch commented, "Epic Australia Pass sales end on June 12, 2024 and are down approximately 22% in units through May 29, 2024, which we believe is primarily a result of the historically poor conditions during the 2023 ski season in Australia. The Epic Australia Pass has grown 43% in units over the past three years." Updated Outlook

|

ropeways.net | Home | Economy | 2024-06-10

Back

Back Add Photos

Add Photos Print

PrintMore articles:

Terry Peak Ski Area: Investing in upgrades to the snowmaking system

2024-07-30

RED Mountain Announces Major Expansion with New Summer Bike Park Project

2024-07-29

Google Adsense